Forming Monopoly in Usa and Actions Agains This

What is a Monopoly?

A monopoly is a market place with a single seller (called the monopolist) simply with many buyers. In a perfectly competitive market, which comprises a large number of both sellers and buyers, no single buyer or seller can influence the price of a article. Dissimilar sellers in a perfectly competitive market, a monopolist exercises substantial control over the market price of a article.

The quantity sold past the monopolist is unremarkably less than the quantity that would be sold in a perfectly competitive firm and the price charged by the monopolist is normally more than the price that would be charged past a perfectly competitive firm. While a perfectly competitive house is a "price taker," a monopolist is a "price maker." Similar to a monopoly is a monopsony, which is a market with many sellers but only 1 buyer.

Understanding Monopoly

A monopolist can raise the price of a production without worrying most the actions of competitors. In a perfectly competitive market place, if a firm raises the price of its products, it will usually lose market share as buyers move to other sellers. Cardinal to agreement the concept of monopoly is understanding this simple statement: The monopolist is the market place maker and controls the amount of a commodity/product available in the market place.

However, in reality, a profit-maximizing monopolist tin't simply charge any price it wants. Consider the following example: Company ABC holds a monopoly over the market for wooden tables and can charge whatever price it wants. Yet, Visitor ABC realizes that if it charged $ten,000 per wooden table, no ane would purchase whatever and the visitor would have to shut downwards. It is because consumers would substitute other commodities such as iron tables or plastic tables for wooden tables.

Thus, Company ABC will accuse the price that enables it to make the maximum profit possible. In order to exercise so, the monopolist must first make up one's mind the characteristics of market demand.

Agreement a Monopolist's Decision

| Quantity (Q) | Price | Total Acquirement (TR) | Average Revenue (AR) | Marginal Acquirement (MR) ∆TR/∆Q |

|---|---|---|---|---|

| TR/Q | ||||

| 1 | 10 | x | ten | 10 |

| 2 | 9 | xviii | nine | 8 |

| 3 | 8 | 24 | 8 | 6 |

| 4 | 7 | 28 | 7 | 4 |

| 5 | 6 | thirty | 6 | 2 |

| 6 | five | 30 | 5 | 0 |

| 7 | 4 | 28 | 4 | -2 |

Consider the post-obit case. Visitor ABC is the sole seller of wooden tables in a pocket-sized boondocks. The table above shows the need bend faced past Company ABC, as well equally the revenue it can earn by selling wooden tables.

The first two columns show the need bend faced past the monopolist. If the monopolist supplies merely one wooden table to the market, it tin can sell that table for $10. If the monopolist produces and supplies ii wooden tables to the market and wants to sell both, it must lower the toll to $9. Similarly, if the monopolist produces and supplies three wooden tables, information technology must lower the cost to $eight to sell all of them.

The 3rd column shows the total acquirement the monopolist tin can earn past selling varying quantities of wooden tables. The 5th cavalcade shows the monopolist's marginal revenue. Information technology is the boosted revenue earned by the monopolist when information technology increases the quantity sold in the market by one unit of measurement.

For a monopolist, the marginal acquirement is always less than or equal to the cost of the article. This arises considering the monopolist is the only seller in the market and, thus, faces a market demand curve that is downward sloping. For example, if Visitor ABC raises production and supply from 3 wooden tables to four wooden tables, its total revenue will increase by just $4, even though it charges $7 per wooden table.

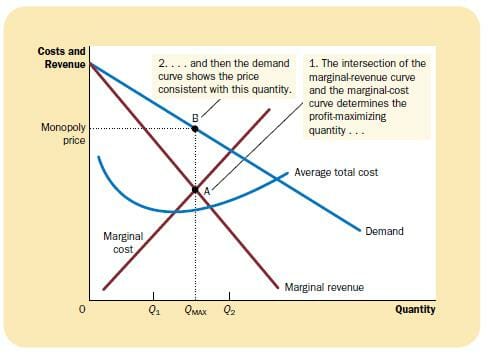

The costs faced by the monopolist depend on the nature of the product process. Consider the example of a monopolist who wants to aggrandize production. The commodity produced past the monopolist requires a large quantity of skilled labor for its product, and skilled labor is in brusque supply.

Thus, as the monopolist raises output, it must pay more than for skilled labor (as skilled labor gets scarcer, it charges a higher toll). Information technology results in the monopolist facing an upward ascension marginal toll curve as shown below.

The monopolist produces that quantity of the commodity that reflects the equilibrium betoken of marginal revenue and marginal cost. The marginal toll is the change in the total cost of production when production is increased past one unit of measurement. The cost charged by the monopolist depends on the market place demand curve.

Source: Principles of Economics by N. Gregor Mankiw

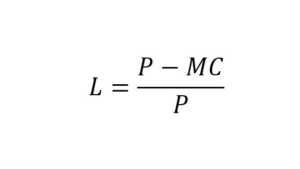

Measuring Monopoly Power – Lerner'southward Index

A common measure out of monopoly power in a market place is provided past Lerner'south Index.

L: Lerner's Alphabetize

P: Cost of the commodity

MC: Marginal cost of the commodity

Related Readings

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)® certification programme, designed to help anyone get a world-class financial analyst. To continue learning and advance your career, see the following complimentary CFI resource:

- Market Economy

- Control Economy

- Law of Supply

- Inelastic Demand

Source: https://corporatefinanceinstitute.com/resources/knowledge/economics/monopoly/

0 Response to "Forming Monopoly in Usa and Actions Agains This"

Post a Comment